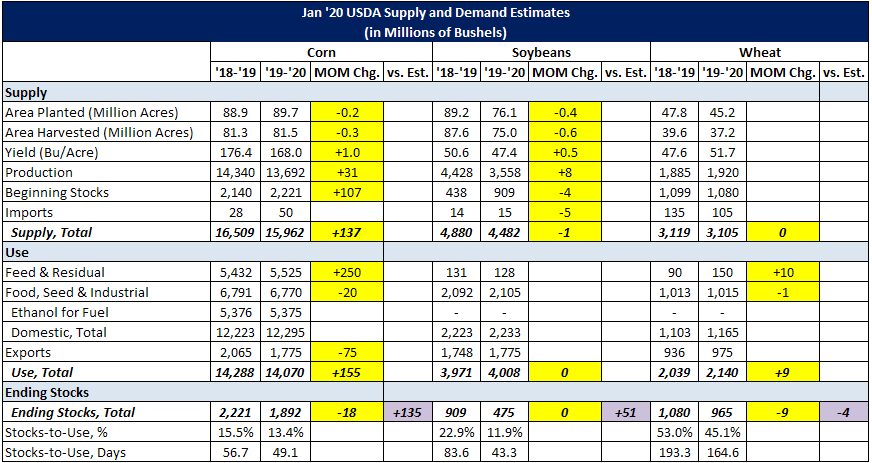

Grain & Oilseeds WASDE Update – Jan ’20

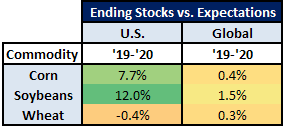

Corn – U.S. and Global Ending Stocks Above Private Estimates

Corn – U.S. and Global Ending Stocks Above Private Estimates

- ’19-’20 U.S. ending stocks of 1.892 billion bushels significantly above expectations

- ’19-’20 global ending stocks of 297.8 million MT slightly above expectations

- ’19-’20 U.S. ending stocks of 475 million bushels significantly above expectations

- ’19-’20 global ending stocks of 96.7 million MT above expectations

- ’19-’20 U.S. ending stocks of 965 million bushels slightly below expectations

- ’19-’20 global ending stocks of 288.1 million MT slightly above expectations